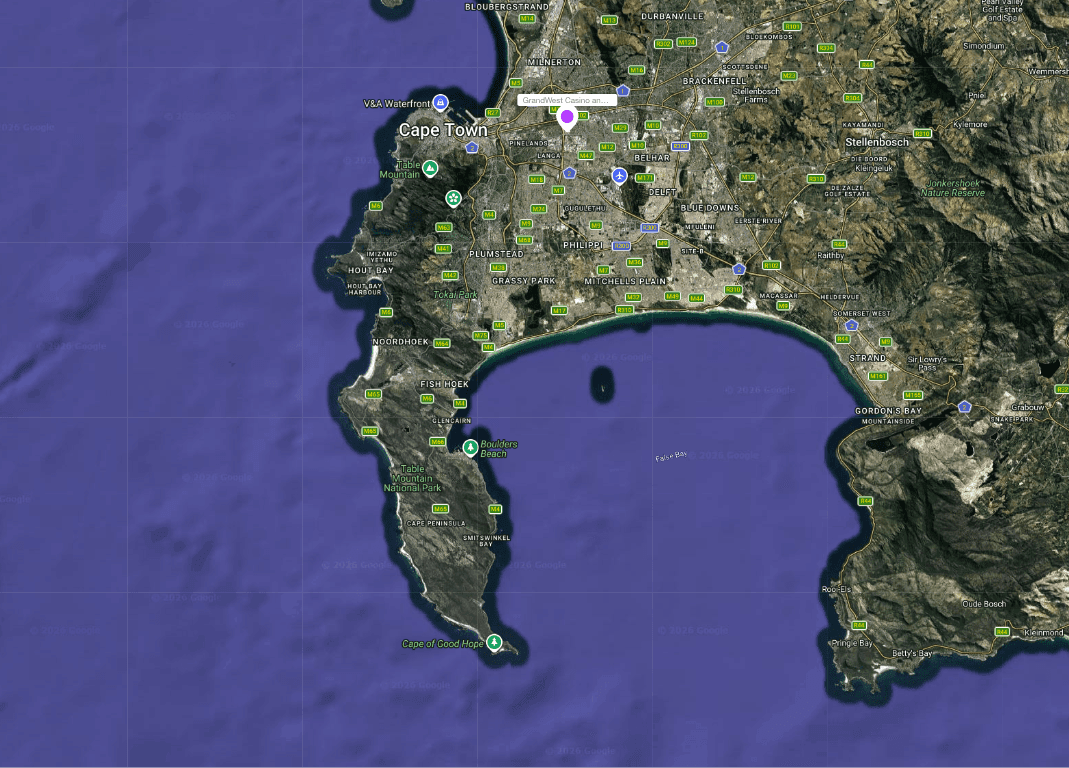

Cape Town’s new R650 million GrandWest Mall development sits less than 10km from Canal Walk, one of Africa’s largest shopping malls. At first glance, the location appears risky. But drive-time catchment analysis tells a very different story. This analysis explores how primary, secondary, and tertiary retail trade areas shape competition, customer accessibility, and mall performance, and why geographic distance alone can be misleading in retail site selection.

Cape Town’s retail landscape is getting another major addition.

Developers have officially broken ground on the new R650 million GrandWest Mall development in Goodwood, anchored by Checkers FreshX and SuperSpar, with the project expected to open in 2027.

At first glance, the location raises an obvious question: why build another major retail center less than 10km from Canal Walk - one of the largest, highest-performing shopping malls in Africa?

On a map, the two locations appear dangerously close.

Geographic Distance Can Be Misleading

Retail competition is rarely determined by straight-line distance alone. What matters is whether a location can access a large, reachable customer base efficiently.

That depends on factors like:

road accessibility

traffic flow

residential concentration

and how far consumers are realistically willing to travel for different retail needs.

Two malls can sit relatively close together geographically while still serving very different trade areas. This is one of the most important concepts in retail site selection and franchise territory planning.

Strong-performing retail catchments are not simply “large” geographically. They are built around a concentrated, reachable customer base with efficient access patterns and sufficient market demand. We explored this idea further in our article on the three factors that shape franchise territory performance, particularly the role customer density and accessibility play in determining territory quality.

The same principle applies to retail site selection.

A location that appears oversaturated on a static map can still perform extremely well if real-world movement patterns create distinct primary trade areas with limited practical overlap.

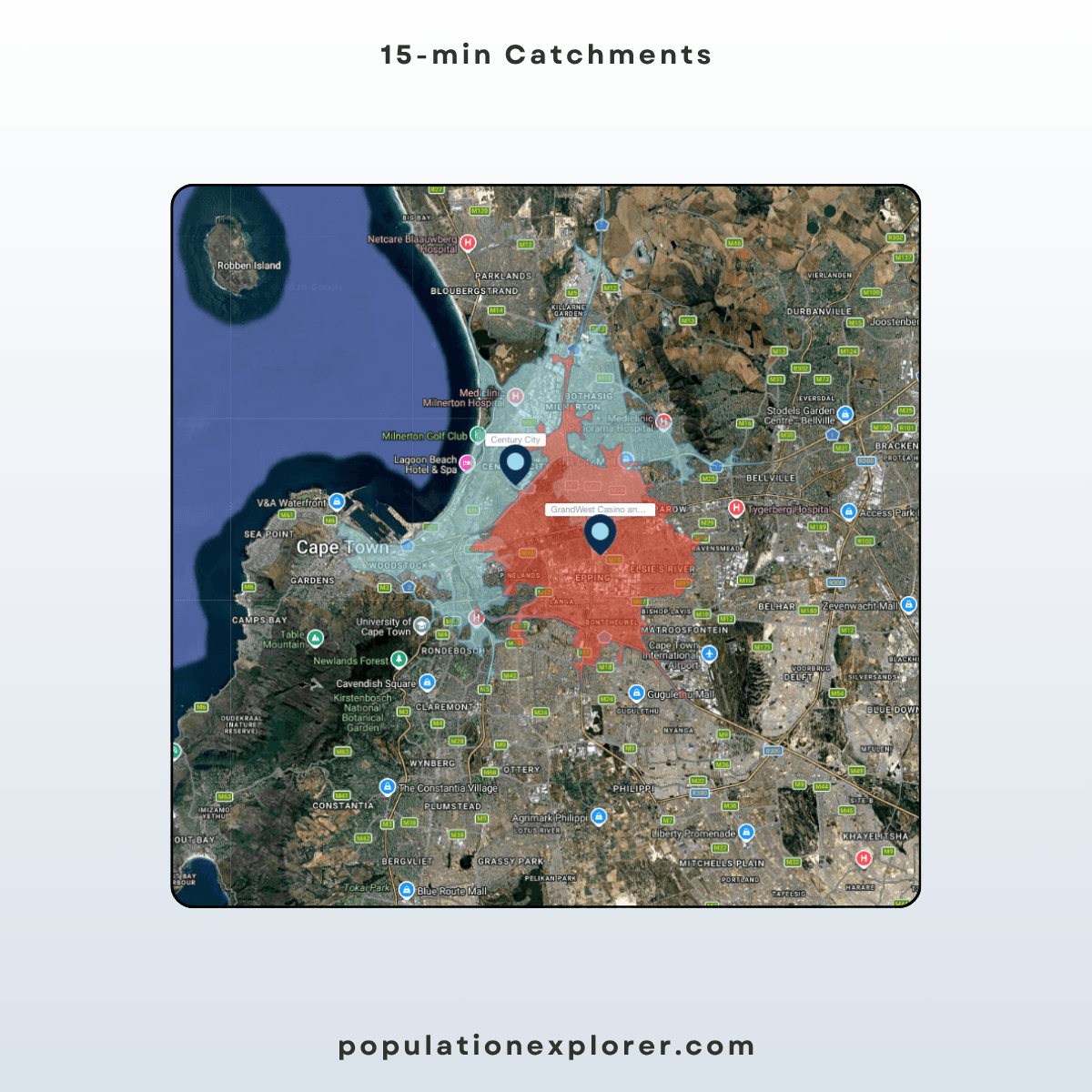

The Primary Catchment: Surprisingly Strong

Using a 15-minute drive-time isochrone as the primary catchment area, the proposed GrandWest Mall location looks exceptionally well-positioned. Despite its proximity to Canal Walk, there is minimal overlap between the two primary trade areas. The road network and movement patterns effectively create two distinct retail ecosystems:

Canal Walk continues to dominate the Century City / Milnerton / Atlantic corridor

while GrandWest captures a different western and north-eastern movement pattern centered around Goodwood, Parow, and surrounding residential density.

In the 15-minute catchment, each mall pulls a strong, ambient population:

GrandWest - 306,170

Canal Walk - 392,201

Ambient populations are those moving, walking around during the day - precisely the population segment malls like this will be prioritizing. From a primary catchment perspective, this does not look like classic cannibalization but rather strategic gap-filling.

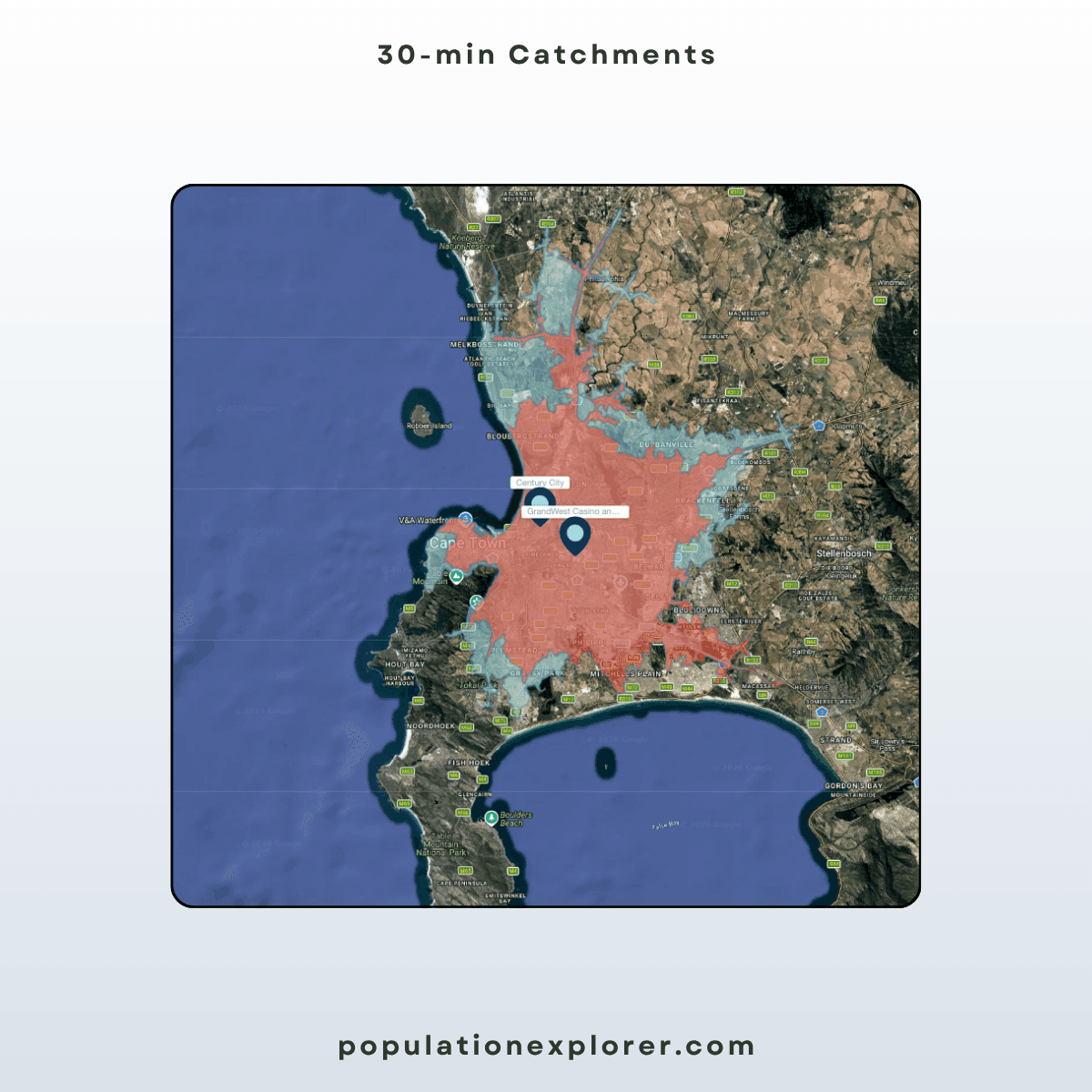

The Secondary Catchment Changes the Story

At the 30-minute drive-time level, overlap increases materially. The two malls begin competing for a much broader regional customer pool, with roughly 50–60% catchment overlap.

This is where the positioning becomes more nuanced.

Secondary catchments often represent:

destination retail trips

weekend shopping behavior

entertainment travel

discretionary spend

higher-order retail choices

At this distance band, Canal Walk’s scale and tenant mix become much more relevant competitive pressures.

This means GrandWest likely succeeds or fails based on whether it can become:

a convenience-first regional center

an entertainment-driven destination

or a differentiated hybrid anchored around casino, leisure, dining, and grocery traffic.

That distinction matters, because competing directly with Canal Walk on “super-regional mall dominance” would be extremely difficult. Canal Walk remains one of the most established retail 'drawcards' in the country, with over 400 stores and massive regional pull.

By 45 Minutes, the Markets Converge

The tertiary catchment tells the broader metropolitan story. At roughly 45 minutes drive-time, overlap appears to reach nearly 95%. At that scale, both malls are competing for the broader Cape Town consumer market. But tertiary catchments are also less predictive of everyday retail behavior.

Most shoppers do not routinely drive 45 minutes for grocery-led retail. Generally, primary catchments predict routine, regular traffic - the majority of transactional behavior - while tertiary catchments define more of the 'destination' traffic, with shoppers visiting for specific products or services on a less frequent basis.

From the standpoint of primary catchments, the GrandWest location appears considerably stronger than many people would assume from simply looking at a map.

The Bigger Retail Trend Beneath This Development

This project also reflects a broader shift in retail development strategy.

Modern mall development increasingly focuses on:

integrated entertainment precincts

grocery-anchored convenience

mixed leisure experiences

and localized accessibility

The GrandWest development appears aligned with that model.

Developers are explicitly positioning the center as an extension of the existing entertainment precinct, integrating retail, dining, casino traffic, and family-focused destinations into a single ecosystem.

That matters because malls no longer compete solely on retail square footage.

They compete on:

frequency of visits

convenience

dwell time

and experiential differentiation.

Final Take

If you only measure this development geographically, the location looks risky. If you measure it through primary catchment behavior, the picture changes dramatically. The low 15-minute overlap suggests the new mall may be serving a meaningful retail gap rather than directly cannibalizing Canal Walk’s core trade area.

The real competitive pressure only begins emerging in the secondary and tertiary catchments, where destination retail behavior becomes more important. That makes this less of a “Canal Walk competitor” and potentially more of a strategically positioned regional complement.

Want to Compare Your Own Retail Catchments?

Most retail competition is shaped by reachable customer bases, not straight-line distance.

Population Explorer helps retail and franchise teams analyze:

drive-time catchments

ambient and residential population

retail overlap

competitor density

and territory accessibility

so expansion decisions can be evaluated using real-world trade areas instead of geography alone.

Analyze your own retail trade area →

Explore expert articles, eCommerce guides, and the latest updates to help your business grow smarter and sell better with Unistore.

Jun 26, 2026

The Cornfield Effect

The cornfield effect is a systematic error in demographic analysis that occurs when census data attributes population to uninhabited areas (e.g., farmland, parks, industrial zones) within a census boundary. This distortion leads to overestimates of customer density and misguided location decisions with notable, negative impacts on franchise territory design and retail site selection. Constrained population models, such as WorldPop Global 2, eliminate the cornfield effect by assigning population only to areas where human settlements have been confirmed to exist.

May 22, 2026

You Can Create a Franchise Territory in Less Than 2 Minutes

Franchise territory mapping no longer has to mean expensive consultants, complex GIS software, or weeks of setup. Modern tools let franchisors create, evaluate, and compare protected territories in minutes.

May 22, 2026

At What Point Does a Franchise Need Territory Mapping?

Not every franchise needs rigorous territory mapping on day one. But once territory decisions begin affecting franchise sales, market protection, expansion planning, and long-term network value, the stakes change quickly.